You're probably here because a deal feels close to done, but something in the title work, payoff statement, or lender requirements suddenly got complicated. A buyer hears there's an old lien. A seller learns a release was never recorded. An agent gets told, “We can't close until this is cleared.” That's the moment priority real estate stops sounding like legal jargon and starts sounding expensive.

Priority is the order in which rights and claims against a property get recognized and paid. If two parties both claim an interest in the same parcel, priority decides who stands first, who waits behind them, and who may get nothing if the value runs out. That order affects closings, refinancing, foreclosure risk, title insurance exceptions, and whether a property is marketable.

Table of Contents

- The Hidden Risk in Every Property Deal

- What Exactly Is Priority in Real Estate

- How Priority Is Established and Recorded

- The Financial and Legal Stakes for All Parties

- Resolving Priority Disputes and Clearing Title

- The Modern Workflow Using AI to Monitor Priority

- Frequently Asked Questions About Real Estate Priority

The Hidden Risk in Every Property Deal

A buyer gets the call two days before closing. The title company found a lien tied to work done years ago by a contractor the current owner barely remembers. The seller insists it was paid. The contractor's company may no longer exist. The lender won't fund until the issue is resolved. The moving truck is booked, the insurance policy is lined up, and everyone who thought this was a routine closing suddenly has a legal problem.

That's how priority shows up in real life. Not as an abstract doctrine, but as a chain reaction. One recorded claim can freeze a sale, delay a refinance, or force a payoff nobody budgeted for.

In a U.S. residential real estate market projected to reach $127.4 trillion by 2029, with active listings up over 71% compared with five years ago, property priority isn't a niche concern. It's basic risk management in a large, active market, as noted in Fixr's real estate statistics and trends.

For people working on the financing side, this issue becomes even more tangible because a lender's security depends on where its mortgage sits in the line of claims. If you want a practical lending-side lens on the subject, Visbanking's overview of commercial real estate lending is a useful companion because it frames how lenders think about collateral, repayment, and exposure.

Why this catches people off guard

Ownership is often assumed to be simple. You buy a home, your name goes on the deed, and the property is yours. Legally, that's incomplete.

Real estate carries a history. Deeds, mortgages, tax claims, easements, judgments, and contractor filings can all attach to the same parcel at different times. Priority is the pecking order that sorts those competing interests.

Practical rule: If a claim appears late in the transaction, that doesn't mean it arose late. It often means nobody checked deeply enough until money was already on the line.

Where the financial pain starts

A priority problem can affect:

- Closing timelines: Funds may be held until a release or payoff arrives.

- Negotiation advantage: The party under deadline often pays more to make the problem go away.

- Financing certainty: A lender may refuse to close unless its lien position is protected.

- Resale value: A clouded title can make future buyers nervous even after a dispute is partly resolved.

It's a simple fact: Many property problems aren't discovered when they happen. They're discovered when someone finally needs clean title.

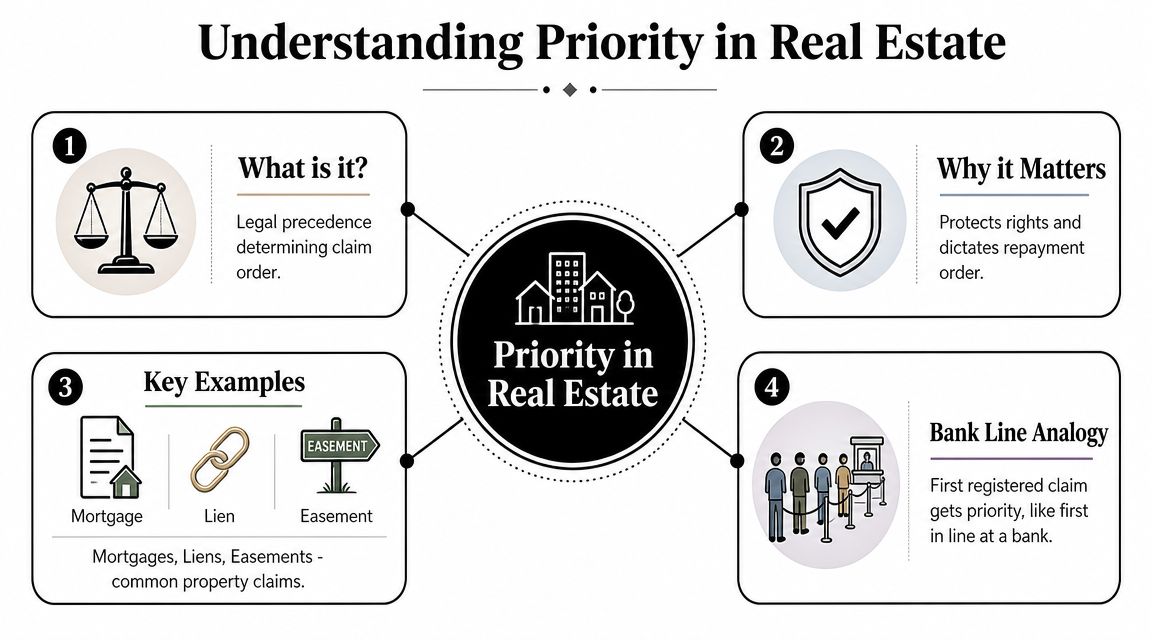

What Exactly Is Priority in Real Estate

Priority is the legal order of competing claims against property. If several people have rights tied to one parcel, the law needs a way to decide whose interest comes first. In practice, that order determines who gets paid first, whose rights are protected first, and whose interest may be wiped out or subordinated.

The simple version of priority

Imagine a line at a bank. The people at the front get served first. Those farther back wait. If the bank runs out of cash, the people at the end of the line may leave with nothing.

Real estate uses a similar logic. The classic shorthand is first in time, first in right. That phrase isn't the whole story, but it gives you the right starting point. A claim that was created and properly recorded earlier will often outrank a later one.

The terms that matter most

A few terms cause confusion because people hear them in closings without getting a plain-English explanation.

- Lien means a claim against property to secure payment of a debt or obligation. A mortgage is a common example. So are tax liens and some contractor claims.

- Encumbrance is broader. It includes liens, but also easements, restrictions, and other burdens that affect the property.

- Title is the legal status of ownership and the bundle of rights attached to the property.

- Conveyancing is the process of transferring real estate from one party to another, including the documents and recordings needed to make that transfer effective.

If you remember one distinction, make it this one. A deed transfers ownership. A title search checks whether that ownership is burdened.

Why recording rules matter

States don't all handle competing claims exactly the same way. Recording statutes are commonly described as race, notice, or race-notice systems. The labels sound technical, but the practical question is straightforward: when two claims conflict, does the law reward speed, lack of knowledge, or both?

Here's the plain-language version:

- In one system, the winner may be the party who records first.

- In another, the winner may be a later party who took without notice of the earlier claim.

- In a combined system, the later party often needs both. No notice and first recording.

A recording system doesn't eliminate disputes. It gives courts and title professionals a rulebook for sorting them.

That's why local recording practice matters so much. The date a document was signed isn't always the only date that matters. The date it was accepted into the public record can become decisive.

A good agent or buyer doesn't need to memorize every statute. But they do need the right mental model. Priority real estate is about order, notice, and proof. Once you understand that, title commitments and exception lists become far less mysterious.

How Priority Is Established and Recorded

A property interest doesn't become practically useful just because someone says it exists. In real estate, rights are protected through documentation, delivery, and recording. That's what turns private agreements into public notice.

Real estate accounted for about 17.5% of U.S. gross state product, and the sector runs on recorded deeds, mortgages, and liens that create stability and predictability, as summarized in The Zebra's real estate statistics research.

What recording actually does

When a deed, mortgage, release, or lien is signed, that's only part of the job. The next step is getting it into the land records maintained by the county or other recording office.

That process usually involves:

- Execution by the parties.

- Submission to the recorder with the required formatting and fees.

- Time-stamping and indexing so others can find it in the public record.

- Retrieval during title review by attorneys, title companies, lenders, or buyers.

Recording does two powerful things. It preserves evidence, and it gives notice to the world. Once a claim is properly recorded, later parties usually can't pretend they had no reason to know it existed.

Common Real Estate Liens and Their Priority

| Lien Type | How It's Created | Typical Priority Rule |

|---|---|---|

| Mortgage lien | Borrower signs loan documents secured by the property, then records them | Earlier recorded mortgages usually rank ahead of later mortgages unless priority is changed by agreement or law |

| Tax lien | Government claim arises from unpaid property taxes or related obligations | Often treated as having superior status and can outrank private liens |

| Judgment lien | Creditor records a judgment against the debtor's real property | Priority commonly depends on when the judgment is properly recorded |

| Mechanic's lien | Contractor, subcontractor, or supplier files based on unpaid work or materials | Priority can depend on state law and may relate to when work began, not only filing date |

| HOA or association lien | Arises under governing documents and applicable statute for unpaid assessments | Priority varies by jurisdiction and may include limited super-priority treatment in some settings |

The table gives the usual logic, not a substitute for state-specific advice. A mechanic's lien is a good example of why broad assumptions can backfire. In some places, it may “reach back” in a way that surprises buyers and lenders who only look at the filing date.

Why paperwork discipline matters

Small administrative errors can create large legal consequences. A release that never gets recorded can leave an old debt appearing active. A misspelled name can make a title search harder. An incorrectly indexed document can delay discovery until closing week.

For teams managing large document volumes, a structured review process is vital. A secure workflow tool such as a private document assistant can help organize title reports, payoff letters, recorded instruments, and correspondence so nothing gets lost between intake and closing.

The practical lesson is simple. Priority isn't created by vibes or verbal assurances. It's created and proven through records.

The Financial and Legal Stakes for All Parties

A priority problem doesn't hit everyone the same way. Each party in a transaction feels it from a different angle, and that's why these disputes become tense so quickly.

What buyers sellers lenders and agents each risk

Buyers care about getting what they thought they were purchasing. If title is clouded by a superior lien or unresolved claim, the buyer may inherit delay, litigation risk, or a property that can't be refinanced cleanly later.

Sellers care about marketability. They may fully believe an old issue was handled years ago, but if the record doesn't show a release, that belief doesn't solve the closing problem. The seller then has to track down proof, negotiate a payoff, or accept escrow holdbacks.

Lenders focus on lien position. A lender making a secured loan wants confidence that its mortgage sits where the underwriting assumed it would sit. If another claim outranks it, the lender's collateral protection weakens immediately.

Agents often get squeezed in the middle. They didn't create the title issue, but clients still expect answers. Missed red flags, overconfident assurances, or a failure to push for early title work can create professional liability exposure.

The cost of a priority issue is rarely just the amount of the lien. It's the delay, leverage loss, legal fees, and financing disruption wrapped around it.

Legal priority and financial priority are not the same

There's another layer that many newer agents miss. Lenders and investors use the word “priority” in an operational sense too. They don't only ask, “Who has first lien position?” They also ask, “What drives the property's ability to carry debt safely?”

For lenders and investors, net operating income, or NOI, is often the most important underwriting metric because it isolates property-level cash generation and feeds directly into valuation through cap rates. A small change in operating expenses can materially shift that valuation, as explained in NetSuite's guide to real estate metrics.

That means a lender may face two priority questions at once:

- Legal priority: Where does the mortgage sit against other claims?

- Financial priority: Does the property itself generate stable income after expenses?

An AI workflow used in adjacent operational fields can help teams think more systematically about triage, documentation, and response timing. For example, the discipline built into an insurance claims agent mirrors what title and lending teams need when exceptions, notices, and supporting documents start arriving from multiple parties.

A clean title position matters. But a lender also cares whether the property can support the deal even after taxes, insurance, maintenance, and vacancy assumptions are tested.

Resolving Priority Disputes and Clearing Title

When a priority issue appears, the worst response is panic. The better response is to treat it like a document problem first, a negotiation problem second, and a lawsuit only if those paths fail.

A practical workflow for curing title problems

Most title defects are addressed through an orderly sequence.

- Read the title report carefully. Don't stop at the label. Find the recording date, instrument number, parties listed, and the exact nature of the claim.

- Confirm whether the claim is still valid. Old liens are often paid but unreleased, assigned to another party, or filed with defects.

- Gather proof. That may include payoff letters, cancelled checks, releases, prior policies, probate papers, or contractor waivers.

- Seek a voluntary resolution. Many disputes end when the claimant signs a release, correction, or payoff agreement.

- Record the cure. A private settlement that never reaches the land records can leave the title cloud in place.

- Litigate if needed. Quiet title actions and related proceedings exist for cases that negotiation can't fix.

When the issue is contested or the claimant is hard to locate, a law firm resource on resolving real estate title defects can help you understand the mechanics of competing interests and quiet title actions before you decide how aggressive the next step should be.

Priority also shapes site selection

Priority isn't only about old paperwork. Astute investors use the term in a strategic sense too. They ask which sites deserve attention first based on location quality, demand signals, and risk-adjusted use.

Modern real estate analytics combines demographics, economic indicators, property attributes, and point-of-interest data to identify sites with the best risk-adjusted use, making priority a strategic question as well as a legal one, as described in Predik Data's overview of real estate analytics.

That broader view matters because title work doesn't happen in a vacuum. A parcel may be legally clear and still be a weak choice. Another may have a curable title issue but sit in a location worth the effort.

Clear title is necessary. It isn't the same thing as a good acquisition.

The strongest operators separate those questions. First, can we own it cleanly? Second, should we want to?

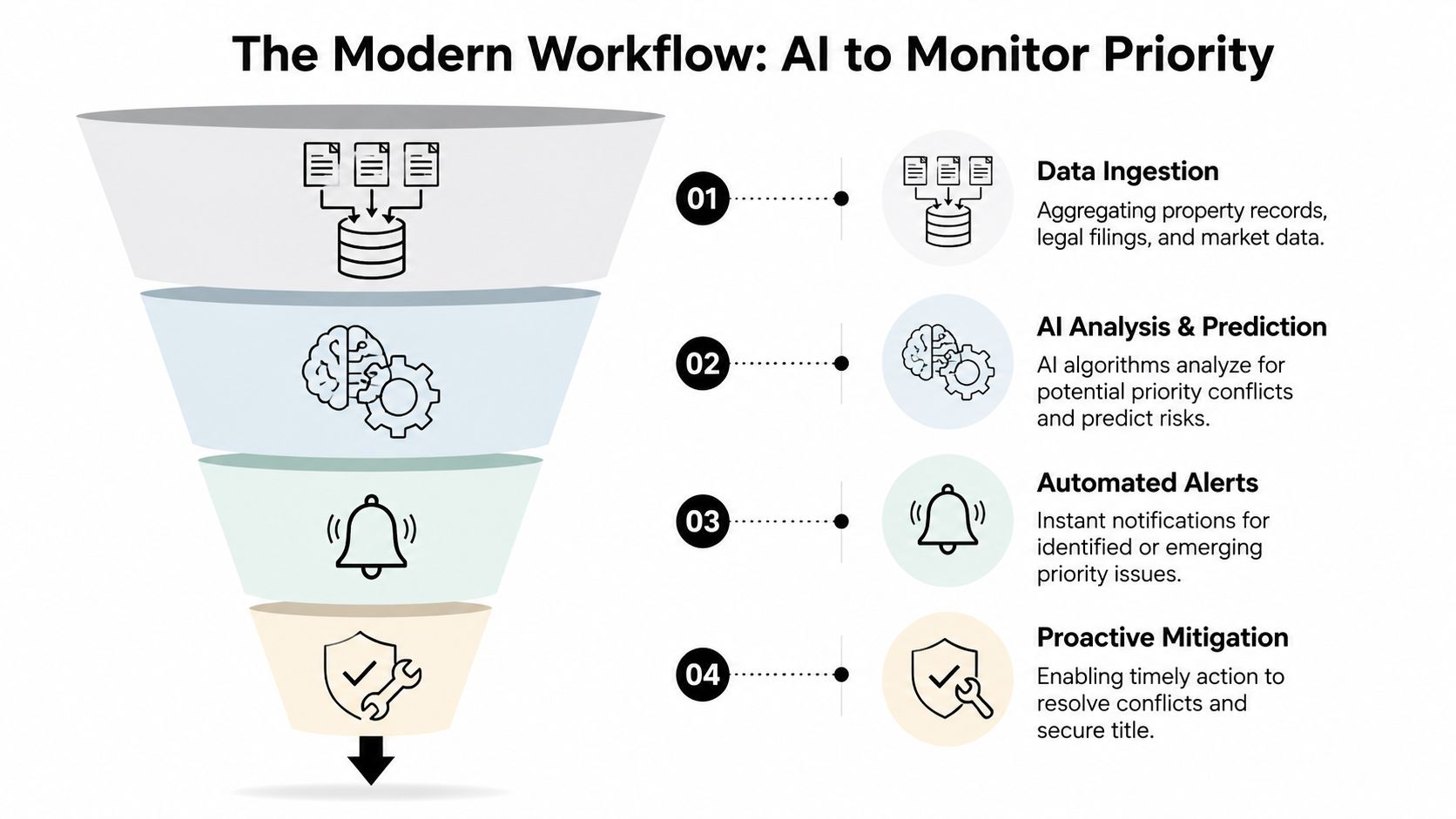

The Modern Workflow Using AI to Monitor Priority

Teams often still treat priority issues as surprise events. They wait for a refinance, listing, or sale to trigger a title search, then scramble through emails and PDFs when a problem surfaces. That's reactive lawyering, reactive brokerage, and reactive asset management.

A better workflow treats title status as something that can be monitored continuously.

From last minute discovery to continuous monitoring

An AI-based process can pull real estate operations closer to how good compliance teams already work. Instead of relying on one stressed closer or paralegal to remember every follow-up, a system can watch for change, route the issue, and preserve the record of what happened next.

That workflow can include county record checks, intake of title updates, extraction of recording data, comparison against an approved property list, and alerts when a new filing appears that affects a parcel in the portfolio.

Here's a short demo on deploying agent-based workflows in practice:

What an AI monitoring workflow can handle

The value isn't magic. It's consistency.

- Portfolio watchlists: An AI employee can monitor a set of addresses, parcel numbers, or borrower names for newly filed instruments that may affect title.

- Document parsing: It can pull key fields from notices, releases, assignments, and title updates so staff don't retype the same details into spreadsheets.

- Alerting: If a mortgage release is still missing, or if a new lien appears before closing, the system can notify the responsible team in Slack or email.

- Compliance logs: Each alert, review, and resolution step can be logged to create an auditable trail.

This turns priority management into an operations problem with defined inputs and outputs. Teams stop relying on memory and inbox archaeology.

For organizations exploring how to set up this kind of process, guidance on deploying AI agents is useful because it shows how monitored workflows, tool connections, and escalation paths can be structured without building everything from scratch.

The legal judgment still belongs to lawyers, title officers, lenders, and decision-makers. AI doesn't replace that. It makes sure the right humans see the right issue early enough to act on it.

Frequently Asked Questions About Real Estate Priority

Can a lien jump ahead of an earlier mortgage

Yes. Some liens get special treatment by statute. Property tax claims are the classic example. Association liens and certain other claims may also receive priority treatment depending on the jurisdiction.

Can you sell a property that has a lien on it

Often yes, but the lien usually must be paid, released, bonded around, or otherwise addressed as part of closing. The exact solution depends on the claim type and whether the title company and lender will accept the proposed cure.

Is a title search the same as title insurance

No. A title search looks for recorded issues. Title insurance allocates risk if a covered title problem later causes loss. One is an investigation. The other is a risk-transfer product.

Can parties change priority by agreement

Sometimes. A subordination agreement is the usual tool. It allows one lienholder to consent to move behind another in priority order.

Does priority real estate ever mean something other than lien order

Yes. In policy and community development discussions, the phrase can point to housing need rather than claim ranking. JPMorgan notes that closing affordable housing gaps requires policy reform and private investment to make projects bankable, which is a different use of the term from title priority, as discussed in JPMorgan's affordable housing analysis.

If you manage closings, loans, or a portfolio of properties, priority issues shouldn't stay hidden until the week money needs to move. Donely gives teams a way to deploy AI employees that can monitor records, route alerts, organize documents, and maintain audit-ready logs from one dashboard. That makes title and compliance work more proactive, more visible, and far easier to manage at scale.